UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, D.C. 20549

FORM 10-K

(Mark One)

| | |

R | | ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the fiscal year ended December 31, 2010

OR

| | |

o | | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the transition period from ___________ to ___________.

Commission File Number: 001-34811

Ameresco, Inc.

(Exact name of registrant as specified in its charter)

| | |

Delaware | | 04-3512838 |

(State or Other Jurisdiction of Incorporation or Organization) | | (I.R.S. Employer Identification No.) |

111 Speen Street, Suite 410 Framingham, Massachusetts | | 01701 |

(Address of Principal Executive Offices) | | (Zip Code) |

(508) 661-2200

(Registrant's Telephone Number, Including Area Code)

Securities registered pursuant to Section 12(b) of the Act:

| |

Title of each class | Name of each exchange on which registered |

Class A Common Stock, par value $0.0001 per share | New York Stock Exchange |

Securities registered pursuant to Section 12(g) of the Act: None

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes o No R

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes o No R

Indicate by check mark whether the Registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the Registrant was required to file such reports) and (2) has been subject to such filing requirements for the past 90 days. Yes R No o

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). Yes o No o

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K is not contained herein, and will not be contained, to the best of Registrant's knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Annual Report on Form 10-K or any amendment to this Annual Report on Form 10-K. o

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer. See definitions of “large accelerated filer,” “accelerated filer” and “smaller reporting company” in Rule 12b-2 of the Exchange Act.

| | | |

Large Accelerated Filer o | Accelerated Filer o | Non-accelerated Filer R | Smaller reporting company o |

| | (Do not check if a smaller reporting company) | |

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Act). Yes o No R

The aggregate market value of the voting and non-voting common equity held by non-affiliates computed by reference to the price at which the common equity was last sold on the New York Stock Exchange on February 28, 2011 was $240,707,811. The registrant has provided this information as of February 28, 2011 because its common equity was not publicly-traded as of the last business day of its most recently completed second fiscal quarter.

Indicate the number of shares outstanding of each of the issuer's classes of common stock as of the latest practicable date.

| |

Class | Shares outstanding as of February 28, 2011 |

Class A Common Stock, $0.0001 par value per share | 23,293,765 |

Class B Common Stock, $0.0001 par value per share | 18,000,000 |

DOCUMENTS INCORPORATED BY REFERENCE

Portions of the definitive proxy statement for our 2011 annual meeting of stockholders are incorporated by reference into Part III.

TABLE OF CONTENTS

NOTE ABOUT FORWARD LOOKING STATEMENTS

This Annual Report on Form 10-K contains “forward-looking statements” within the meaning of Section 21E of the Securities Exchange Act of 1934, as amended, or the Exchange Act. All statements, other than statements of historical fact, including statements that refer to projections regarding our future financial performance, our anticipated growth and trends in our businesses, our future capital needs and capital expenditures; our future market position and competitive changes in the marketplace for our services; our ability to integrate new technologies into our services; our ability to access credit or capital markets; our reliance on subcontractors; potential acquisitions or divestitures; the continued availability of key personnel; and other characterizations of future events or circumstances are forward-looking statements. These statements are often, but are not exclusively, identified by the use of words such as “may,” “will,” “expect,” “believe,” “anticipate,” “intend,” “could,” “estimate,” "target,” “project,” “predict” or “continue,” and similar expressions or variations. These forward-looking statements are based on current expectations and assumptions that are subject to risks, uncertainties and other factors that could cause actual results and the timing of certain events to differ materially and adversely from the future results expressed or implied by such forward-looking statements. Risks, uncertainties and factors that could cause or contribute to such differences include, but are not limited to, those discussed in the section titled “Risk Factors,” set forth in Item 1A of this Annual Report on Form 10-K and elsewhere in this report. The forward-looking statements in this Annual Report on Form 10-K represent our views as of the date of this Annual Report on Form 10-K. Subsequent events and developments may cause our views to change. However, while we may elect to update these forward-looking statements at some point in the future, we have no current intention of doing so except to the extent required by applicable law. You should, therefore, not rely on these forward-looking statements as representing our views as of any date subsequent to the date of this Annual Report on Form 10-K.

This Annual Report on Form 10-K also contains estimates made by independent parties and by us relating to market size and growth and other industry data. These estimates involve a number of assumptions and limitations and you are cautioned not to give undue weight to such estimates. In addition, projections, assumptions and estimates of our future performance and the future performance of the industries in which we operate are necessarily subject to a high degree of uncertainty and risk due to a variety of important factors, including those described in “Risk Factors” and “Management's Discussion and Analysis of Financial Condition and Results of Operations” in Item 1A and Item 7, respectively, in this report. These and other factors could cause results to differ materially and adversely from those expressed in the estimates made by the independent parties and by us.

PART I

Item 1. Business

Company Overview

Ameresco is a leading provider of energy efficiency solutions for facilities throughout North America. Our solutions enable customers to reduce their energy consumption, lower their operating and maintenance costs and realize environmental benefits. Our comprehensive set of services addresses almost all aspects of purchasing and using energy within a facility. Our services include upgrades to a facility's energy infrastructure and the construction and operation of small-scale renewable energy plants. As one of the few large, independent energy efficiency service providers, we are able to objectively select and provide the products and technologies best suited for a customer's needs. Having grown from four offices in three states in 2001 to 56 offices in 29 states and five Canadian provinces by year-end 2010, we now combine a North American footprint with strong local operations, which enable us to remain close to our customers and serve them effectively. We believe that we are a leading provider of energy efficiency solutions for facilities throughout North America based on having secured more than 30%, by value, of the projects awarded from October 1, 2008 through December 2010 under U.S. Department of Energy programs related to energy savings performance contracts, as well as our belief based on our own internal analyses and on third-party analyst reports that, by revenue, we are among the top ten North American energy services companies/energy consultants.

The market for energy efficiency services has grown significantly over the last 20 years, driven largely by rising and volatile energy prices, advances in energy efficiency and renewable energy technologies, governmental support for energy efficiency and renewable energy programs and growing customer awareness of energy costs and environmental issues. End users and governmental agencies are increasingly viewing energy efficiency measures as a cost-effective solution for saving energy, renewing aging facility infrastructure and reducing harmful emissions.

Our principal service is the development, design, engineering and installation of projects that reduce the energy and operations and maintenance, or O&M, costs of our customers' facilities. These projects typically include a variety of measures customized for the facility and designed to improve the efficiency of major building systems, such as heating, ventilation, air conditioning and lighting systems. We typically commit to customers that our energy efficiency projects will satisfy agreed upon performance standards upon installation or achieve specified increases in energy efficiency. In most cases, the forecasted

lifetime energy and operating cost savings of the energy efficiency measures we install will defray all or almost all of the cost of such measures. In many cases, we assist customers in obtaining third-party financing for the cost of constructing the facility improvements, resulting in little or no upfront capital expenditure by the customer. After a project is complete, we may operate, maintain and repair the customer's energy systems under a multi-year O&M contract, which provides us with recurring revenue and visibility into the customer's evolving needs.

We also serve certain customers by developing and building small-scale renewable energy plants located at or close to a customer's site. Depending upon the customer's preference, we will either retain ownership of the completed plant or build it for the customer. Most of our small-scale renewable energy plants to date have been constructed adjacent to landfills and use landfill gas, or LFG, to generate energy. Our largest renewable energy plant is currently under construction and will use biomass as the source of energy. In the case of the plants that we own, the electricity, thermal energy or processed LFG generated by the plant is sold under a long-term supply contract with the customer, which is typically a utility, municipality, industrial facility or other large purchaser of energy. We also sell and install photovoltaic, or PV, panels and integrated PV systems that convert solar energy to power. By enabling our customers to procure renewable sources of energy, we help them reduce or stabilize their energy costs, as well as realize environmental benefits.

We provide our services primarily to governmental, educational, utility, healthcare and other institutional, commercial and industrial entities. Since our inception in 2000, we have served more than 2,000 customers.

Our revenue has increased from $20.9 million in 2001, our first full year of operations, to $618.2 million in 2010. We achieved profitability in 2002 and have been profitable every year since then.

As of December 31, 2010, we had backlog of approximately $651 million in future revenue under signed customer contracts for the installation or construction of projects, which we sometimes refer to as fully-contracted backlog; and we also had been awarded projects for which we do not yet have signed customer contracts with estimated total future revenue of an additional $483 million. As of December 31, 2009, we had backlog of approximately $598 million in future revenue under signed customer contracts for the installation or construction of projects; and we also had been awarded projects for which we had not yet signed customer contracts with estimated total future revenue of an additional $706 million. The contracts reflected in our fully-contracted backlog typically have a construction period of 12 to 24 months; this is the period over which we expect to recognize revenue for customer contracts. Where we have been awarded a project, but have not yet signed a customer contract for that project, which we sometimes refer to as awarded projects, we would not begin recognizing revenue unless a customer contract has been signed and we treat the project as fully-contracted backlog. Historically, awarded projects typically have taken 6 to 12 months to result in a signed contract and thus convert to fully-contracted backlog. It may take longer, however, depending upon the size and complexity of the project. Revenue generated from backlog was $507 million in 2010. See "We may not recognize all revenue from our backlog or receive all payments anticipated under awarded projects and customer contracts" in Item 1A, Risk Factors.

We also expect to realize recurring revenue both under long-term O&M contracts and under energy supply contracts for renewable energy plants that we own. In addition, we expect to generate revenue from solar and other product and service sales. Revenue generated from O&M, energy supply contracts and solar and other product and service sales was $111 million in 2010.

Industry Overview

Energy efficiency companies, sometimes referred to as energy services companies, or ESCOs, develop, install and arrange financing for projects designed to improve the energy efficiency of buildings and other facilities. Typical products and services offered by energy efficiency companies include boiler and chiller replacement, HVAC upgrades, lighting retrofits, equipment installations, on-site cogeneration, renewable energy plants, load management, energy procurement, rate analysis, risk management and billing administration. Energy efficiency companies often offer their products and services through energy savings performance contracts, or ESPCs. Under these contracts, energy efficiency companies assume certain responsibilities for the performance of the installed measures, under assumed conditions, for a portion of the project's economic lifetime.

Energy Efficiency

The market for energy efficiency services has grown significantly, driven largely by rising and volatile energy prices, advances in energy efficiency and renewable energy technologies, governmental support for energy efficiency and renewable energy programs and growing customer awareness of energy and environmental issues. End users, utilities and governmental agencies are increasingly viewing energy efficiency measures as a cost-effective solution for saving energy, renewing aging facility infrastructure and reducing harmful emissions.

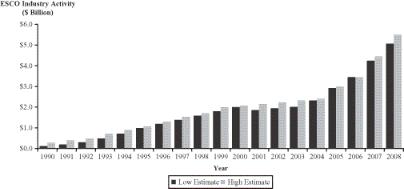

According to a 2008 Frost & Sullivan report, as shown in the table below, activity by ESCOs in the North American market for energy management services, including energy efficiency, demand response and other services, grew at a compound annual growth rate, or CAGR, of 22% from 2004 through 2008, with the estimated size of the market reaching more than $5 billion in 2008:

In a 2009 report, McKinsey & Company estimated that energy savings worth $1.2 trillion are available if the full amount of economically viable and commercially available energy efficiency potential is implemented in the United States through 2020, which would require upfront investment of $520 billion.

The U.S. federal government has significantly increased its interest in and spending on energy efficiency measures over the past decade. Legislation authorizing federal agencies to enter into ESPCs was originally passed in 1992, and in 2007, three years after the sunset of the original legislation, Congress passed new ESPC legislation without a sunset provision. As of March 2010, ESPCs have been awarded by 25 different federal agencies and departments in 49 states, resulting in more than 550 federal energy efficiency projects cumulatively worth $3.6 billion. In December 2008, the U.S. Department of Energy awarded new Indefinite Delivery, Indefinite Quantity, or IDIQ, contracts that permit 16 companies to propose and procure ESPCs with federal agencies. Of these 16 companies, only three are independent companies not affiliated with an equipment manufacturer, utility or fuel company. In December 2010, new streamlined qualification-based competition procedures applicable only to energy savings performance contracting were enacted. We believe the new competition procedures better reflect the unique characteristics of the contracting process, and should allow for a quicker contractor selection process.

There are three principal types of energy efficiency companies:

| |

• | Independent Energy Services Companies — Energy efficiency companies not associated with an equipment manufacturer, utility or fuel company. Most of these companies are small and focus either on a specific geography or specific customer base. |

| |

• | Utility Affiliated Energy Services Companies — Companies owned by regulated North American utilities, many of which were traditionally focused on the service territories of their affiliated utilities. Many of these companies have since expanded their geographical markets. Examples include Constellation Energy Projects and Services and ConEdison Solutions. |

| |

• | Equipment Manufacturers — Companies owned by building equipment or controls manufacturers. Many of these companies have a national presence through an extensive network of branch offices. Examples include Honeywell, Johnson Controls and Siemens. |

Renewable Energy

Utilities and large purchasers of energy are increasingly seeking to use renewable sources of energy, such as LFG, wind, biomass, geothermal and solar, to reduce or stabilize their energy costs, meet regulatory mandates for use of renewable energy, diversify their fuel sources and realize environmental benefits, such as the reduction of greenhouse gas emissions.

According to the International Energy Agency, utilities worldwide are expected to increase their overall renewable generation capacity (excluding hydro) as a percentage of their overall capacity from less than four percent in 2007 to 13% in 2030.

Industry Trends

We believe the following trends and developments are driving the growth of our industry.

| |

• | Rising and Volatile Energy Prices. Over the past decade, energy linked commodity prices, including oil, gas, coal and electricity, have all increased and exhibited significant volatility. From 1999 to 2009, average U.S. retail electricity prices have increased by more than 50%. Over an 18 month period from January 2007 to July 2008, oil prices increased by almost 200%. According to the U.S. Energy Information Administration, or EIA, oil prices are expected to increase by approximately 115% from 2009 to 2035 and electricity prices are expected to increase by approximately six percent annually over the same time period. We believe that rising energy prices combined with significant volatility have resulted in growing demand for energy efficiency measures that reduce energy usage and for sources of renewable energy that can stabilize energy costs. |

| |

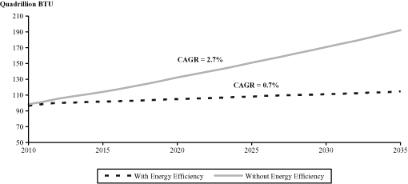

• | Potential of Energy Efficiency Measures to Significantly Reduce Energy Consumption. According to the EIA, U.S. energy demand is expected to increase nearly twofold from 2010 to 2035 in the absence of any improvements in energy efficiency, but the implementation of energy efficiency measures can significantly reduce energy consumption, as shown below: |

Total U.S. Energy Consumption

According to a July 2009 report by McKinsey & Company, economically viable and commercially available energy efficiency measures, if fully implemented, have the potential to save more than one trillion kWh of electricity, or 23% of overall U.S. demand, by 2020.

| |

• | Aging and Inefficient Facility Infrastructure. Many organizations continue to operate with an energy infrastructure that is significantly less efficient and cost effective than what is currently available through more advanced technologies applied to lighting, heating, cooling and other building systems. As these organizations explore alternatives for renewing their aging facilities, they often identify multiple areas within their facilities that could benefit from the implementation of energy efficiency measures, including the possible use of renewable sources of energy. According to a July 2009 report by McKinsey & Company, increased energy efficiency through facility renewal of government buildings, community infrastructure and existing homes in the United States represents a $76 billion market opportunity through 2020, and could result in energy savings of $174 billion over the same period. |

| |

• | Increased Focus on Cost Reduction. The current economic environment has led many organizations to search for opportunities to reduce their operating costs. There has been a growing awareness that reduced energy consumption presents an opportunity for significant long-term savings in operating costs and that the installation of energy efficiency measures can be a cost-effective way to achieve such reductions. |

| |

• | Movement Toward Industry Consolidation. As energy efficiency solutions continue to increase in technological complexity and customers look for service providers that can offer broad geographic and product coverage, we believe smaller niche energy efficiency companies will continue to look for opportunities to combine with larger companies that can better serve their customers’ needs. In addition, we believe utilities will continue to consider divesting their energy management services divisions, in part because of the potential conflicts between the interests of an energy provider and the interests of a provider of energy efficiency services. Increased market presence and size of energy efficiency companies should, in turn, create greater customer awareness of the benefits of energy efficiency measures. |

| |

• | Increased Use of Third-Party Financing. Many organizations desire to use their existing sources of capital for core investments or do not have the internal capacity to finance improvements to their energy infrastructure. These organizations often require innovative structures to facilitate the financing of energy efficiency and renewable energy projects. Customers seeking to upgrade or renew their energy systems are increasingly seeking to enter into ESPCs or other creative arrangements that facilitate third-party financing for their projects. |

| |

• | Increasing Legislative Support and Initiatives. In the United States and Canada, federal, state, provincial and local governments have enacted and are considering legislation and regulations aimed at increasing energy efficiency, reducing greenhouse gas emissions and encouraging the expansion of renewable energy generation. Examples of such legislation and regulation are: |

| |

• | Federal. In 2007, the United States enacted the Energy Independence and Security Act which mandates that federal buildings reduce energy consumption by 30% by 2015 compared to their 2003 baseline and contains multiple provisions promoting long-term ESPCs. The U.S. Department of Energy also has a number of research, development, grant and financing programs — most notably the DOE Loan Guarantee Program — to encourage energy efficiency and renewable energy. Additionally, the United States has adopted federal incentives for renewable energy, including the production tax credit, investment tax credit and accelerated depreciation. |

| |

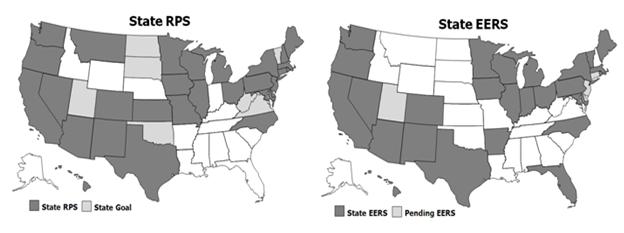

• | States. At the U.S. state level, significant measures to support energy efficiency and renewable energy have been implemented, including as of December 31, 2010, the following: |

| |

• | 26 states have adopted energy efficiency resource standards, or EERS, and long-term energy savings targets for utilities. |

| |

• | 29 U.S. states and the District of Columbia have renewable portfolio standards, or RPS, in place, and seven states have renewable portfolio goals. |

| |

• | 22 states have passed legislation enabling a new financing mechanism known as Property Assessed Clean Energy (PACE) Bonds. The bonds provide funds that can be used by commercial and residential property owners to finance efficiency measures and small-scale renewable energy systems. |

| |

• | The U.S. Senate and House of Representatives have passed various forms of EERS and RPS legislation and, if enacted, all 50 states would have additional incentives to support energy efficiency and renewable energy. |

| |

• | Canada. The federal, provincial and local governments have also provided incentives for the development of energy efficiency and renewable energy projects, and facility renewal. In 2010, the federal government announced its 2020 greenhouse gas emissions reduction target under the Copenhagen Accord, a 17% reduction from 2005 levels, subject to adjustment to remain consistent with the U.S. target. In 2009, Ontario and Quebec both passed enabling legislation to establish cap-and-trade programs, which aim at reducing emissions by 15% below 1990 levels by 2020 and 20% by 2020, respectively. Ontario also passed the Green Energy and Green Economy Act in May 2009 to expand renewable energy production, encourage energy conservation and create green jobs. The act established a feed-in tariff program with pricing incentives to encourage the development of renewable energy. Similarly, British Columbia has also passed enabling legislation to establish a cap-and-trade program and a greenhouse gas reduction target of at least 33% below 2007 levels by 2020. Under the federal Economic Action Plan, the federal government has committed to multi-year expenditures of $4 billion for new infrastructure funding, and has established program funds of $1 billion for sustainable energy and other green projects and $2 billion to repair, retrofit and expand facilities at post-secondary institutions. |

| |

• | Economic Stimuli. Governments worldwide have allocated significant portions of economic stimuli to clean energy. The American Recovery and Reinvestment Act of 2009 allocated $67 billion to promote clean energy, energy efficiency and advanced vehicles. Additionally, the Emergency Economic Stabilization Act instituted a grant program that provides cash in lieu of the investment tax credit for eligible renewable energy generation sources which commence construction in 2010. |

These trends and developments are contributing to the growth of the market for energy efficiency and renewable energy solutions and create opportunities for energy efficiency companies that can provide the comprehensive range of services and deep level of expertise necessary to cost-effectively meet customers’ energy and facility renewal needs.

The Ameresco Solution

Ameresco’s solutions enable customers to increase energy efficiency, reduce costs and realize environmental benefits. Our comprehensive set of services addresses almost all aspects of purchasing and using energy within a facility. We have significant in-house expertise in identifying, designing and installing the improvements necessary to enhance the energy efficiency of a facility. As an independent company unaffiliated with any specific equipment manufacturer or utility, we have the freedom and flexibility to be objective in selecting, purchasing and integrating the particular systems best suited for a facility’s infrastructure.

We can reduce our customers’ energy costs in several ways. The energy efficiency measures that we design, install and manage, such as boilers, chillers, lighting systems and control systems, can reduce the usage of energy and water, thereby significantly reducing operating costs. By upgrading aging facilities, we can also significantly reduce ongoing O&M costs. In addition, customers buying energy from our renewable energy plants can reduce or stabilize their energy prices under 10- to 20-year supply contracts with us. We also sell and install equipment, such as solar energy products, that enable customers to benefit from federal and state tax credits and other governmental incentives.

Most customers undertaking an energy efficiency project desire to minimize their upfront costs and overall cost of system ownership. We assist customers in achieving their economic objectives by helping to arrange third-party financing, which often results in little or no upfront capital expenditure by the customer. By committing that our energy efficiency measures will achieve specified performance standards upon installation or specified increases in energy efficiency over a multi-year period, we enable our customers to reduce the risk that the systems we install will not achieve forecasted energy usage savings. In most cases, the forecasted lifetime savings of the energy efficiency measures we install will defray all or almost all of the cost of such measures. For customers desiring to procure renewable energy sources, we provide financing flexibility by offering either to build a small-scale renewable energy plant that will be owned and financed by the customer itself or to build and finance a plant that we will own and that will supply energy or gas to the customer under a long-term contract.

Our solutions also assist our customers in achieving their environmental goals and, in the case of governmental customers, complying with federal and state energy efficiency and emission reduction mandates. Our energy efficiency improvements enable customers to achieve environmental benefits both by reducing their energy and water usage and by reducing their reliance on conventional energy sources. Customers procuring electricity, thermal energy or processed gas from the renewable energy plants that we construct can further reduce their emissions of greenhouse gases and other pollutants.

Our Competitive Strengths

We believe our competitive strengths include the following:

| |

• | One Stop, Comprehensive Service Provider. We offer our customers expertise in addressing almost all aspects of purchasing and using energy within a facility. Our experienced project development and engineering staff provide us with the capability and flexibility to determine the combination of energy efficiency measures that is best suited to achieve the customer's energy efficiency and environmental goals. Our solutions range from smaller projects, such as a lighting system retrofit, to larger and more complex projects comprising new heating, cooling and electrical infrastructure, solar panels and a small-scale renewable energy plant serving multiple buildings. |

| |

• | Independence. We are an independent company with no affiliation to any equipment manufacturer, utility or fuel company. Unlike affiliated service companies, we have the freedom and flexibility to be objective in selecting particular products and technologies available from different manufacturers. By combining components from multiple sources, we can optimize our solution for customers' particular needs. In addition, we can leverage the high volume of equipment purchases that originate across our North American operations to obtain attractive pricing terms that enable us to provide cost effective solutions to our customers. |

| |

• | Strong Customer Relationships. We have served over 2,000 customers since our inception, including over 1,000 customers in 2010. The sales, design and construction process for energy efficiency and renewable energy projects typically takes from 12 to 36 months, during which time our engineers work closely with the customer to ensure a successful installation. For certain projects, we enter into a multi-year O&M contract under which we have personnel on site monitoring and controlling the customer's energy systems. Our services include helping customers procure energy and managing their utility bill payment processes. All of these design, engineering and support activities foster a close relationship with our customers, which positions us to identify their future needs and provide additional services to them. For example, for a single federal facility, we have completed three separate projects over the period from 2005 to 2009. |

| |

• | Creative Solutions. We seek to provide innovative solutions to meet our customers’ energy efficiency, facility renewal and environmental goals. Our engineering staff has expertise in a broad range of technologies and energy savings strategies encompassing different types of electrical, heating, cooling, lighting, water, renewable energy, and other facility infrastructure systems. We are constantly seeking to identify new services, products and technologies that can be incorporated into our energy efficiency and renewable energy solutions to enhance their performance. We apply this expertise to design and engineer innovative solutions customized to meet the specific needs of each client. We also have an internal structured finance team that is skilled and experienced in arranging third-party financing for our customers’ projects. |

| |

• | Strong National and Local Presence. We have a nationwide presence in both the United States and Canada and serve certain of our customers in European locations. We maintain a centralized staff of engineering, financial and legal personnel at our headquarters in Massachusetts, who provide support to our eight regional offices and 47 other field offices located throughout the United States and Canada. We leverage our centralized resources and local offices by sharing experiences and best practices across the offices. We are able to maintain an entrepreneurial approach toward our customers by delegating significant responsibility to our regional offices and making them accountable for their own operational and financial performance. We believe that our organizational structure enables us to be fast, flexible and cost effective in responding to our customers’ needs. |

| |

• | Experienced Management and Operations Team. Our executive officers have an aggregate of over 150 years of experience in the energy efficiency field. Some have worked together for over 15 years and most have worked together at Ameresco for over five years. In addition, we have accumulated significant in-house expertise in our sales, engineering, financing, legal, construction and operations functions. As of December 31, 2010, we employed over 200 engineers, whose experience with respect to fuels, rates, technologies and geography specific regulation and economic benefits enables us to propose and design energy efficiency solutions that take into account the economic, technological, environmental and regulatory considerations that we believe underlie the cost efficiencies and operational success of a project. Many of our employees were previously employed by utilities, construction companies, financial institutions, engineering firms, consultancies and government agencies, which provides them with specialized experience in solving problems and creating value for our customers. |

| |

• | Federal and State Qualifications. The federal governmental program under which federal agencies and departments can enter into ESPCs requires that energy service providers have a track record in the industry and meet other specified qualifications. Over 20 states require similar qualifications to do business with state agencies and, in certain cases, with other governmental agencies in the state. In 2008, we renewed our IDIQ qualification under the U.S. Department of Energy program for ESPCs, and we are currently qualified to enter into ESPCs in most states that require qualification. Our projects accounted for almost 40 percent of the total dollar amount of published task orders issued under the Department of Energy’s IDIQ program for ESPCs in fiscal 2010. The scope of our qualifications provides us with the opportunity to continue to grow our business with federal, state and other governmental customers and differentiates us from energy efficiency companies that have not been similarly qualified. |

| |

• | Integration of Strategic Acquisitions. We have a track record of completing over ten acquisitions that have enabled us to broaden our offerings, expand our geographical reach and accelerate our growth. We follow a disciplined approach in evaluating and valuing potential acquisition candidates and frequently improve their operating performance significantly following our acquisition. Our acquisition of the energy services business of Duke Energy in 2002 expanded our geographical reach into Canada and the southeastern United States, and enabled us to penetrate the federal government market for energy efficiency projects. Our acquisition of the energy services business of Northeast Utilities in 2006 further grew our capability to provide services for the federal market and in Europe. Our acquisition of Southwestern Photovoltaics in 2007 significantly expanded our offering of solar energy products and services. In 2010, we acquired Quantum Engineering and Development, an energy services company, in order to expand our footprint into the Pacific Northwest. We believe that our ability to offer a comprehensive set of energy efficiency services across North America has been, and will continue to be, enhanced by our expertise in identifying and completing acquisitions that expand our service offerings, as well as by our ability to integrate and leverage the skilled engineering, sales and operational personnel that come to us through these acquisitions. |

Strategy

Our goal is to capitalize on our strong customer base and broad range of service offerings to become the leading provider of comprehensive energy efficiency and renewable energy solutions.

Key elements of our strategy include the following:

| |

• | Continue to Maintain Customer Focus. Our success will continue to depend in large part on our ability to understand and meet our customers' energy infrastructure requirements. We will maintain an entrepreneurial approach toward our customers and remain flexible in designing projects tailored specifically to meet their needs. We will also continue to monitor and explore alternative services, products and technologies that might offer improved system performance and will seek to design and engineer innovative solutions for our customers. |

| |

• | Execute in a Timely and Cost-Effective Manner. For existing business, we will focus on executing all ongoing contracts in a timely and cost-effective manner while maintaining high customer satisfaction ratings. |

| |

• | Maintain Cost Control. We plan to focus on maintaining operating expenses, overhead in particular, within a manageable percent of sales range as the Company continues to grow. |

| |

• | Increase Market Penetration and Expand our Footprint. We plan on continuing to focus on increasing our success rates on customer proposals, pursue organic growth, expand the scope of product and service offerings, and focus on growing through select strategic acquisitions. |

| |

• | We believe we can increase our success rate on customer proposals by leveraging our expertise in designing, engineering and installing energy efficiency solutions in order to drive the request for proposal, or RFP, process. Based upon our experience, actively driving the RFP process leads to a higher success rate. |

| |

• | We also expect to continue to expand our North American footprint organically by hiring additional salespeople and opening three to four new offices during 2011 in locations where we have identified existing and potential opportunities. Our plans may include regions outside of North America as well. |

| |

• | We plan to continue to expand our offerings by implementing new types of energy efficiency services, products and improvements to complement existing products and leverage in-house expertise. We believe this should also help build our competitive advantage. |

| |

• | We have been able to accelerate the expansion of our service offerings, customer base and geographic reach through targeted acquisitions. We expect that we will continue to follow a disciplined approach in evaluating and valuing potential acquisition candidates. We plan to pursue strategic bolt-on and fill-in acquisitions that we believe are accretive and enable us to both expand geographically and broaden our product and service offerings. |

| |

• | Increase Recurring Revenue from O&M. We intend to continue to seek opportunities to increase our sources of recurring revenue. For many of our energy efficiency projects, we enter into multi-year O&M contracts, and we plan to continue to grow both the number and scope of such contracts. |

| |

• | Continue to Invest in Renewable Energy Projects. We currently obtain recurring revenue from sales of electricity, thermal energy and gas generated by the small-scale renewable energy and central plants that we construct and own, and we plan to continue to seek opportunities to construct such plants based on LFG, biomass, biogas, solar, wind, geothermal and other sources of energy going forward. All of the renewable projects that we pursue must satisfy our internal metrics for potential returns. |

| |

• | Improve Margins and Key Metrics for All Businesses. We will continue to focus on higher quality backlog and recurring revenue from O&M and small-scale renewable energy projects. We believe doing so should help improve gross margins, operating margins and EBITDA margins over time. We will also continue to maintain our internal focus on proposals, success rates, backlog, revenue growth and customer satisfaction. |

Ameresco’s Products and Services

We offer a comprehensive set of services that includes the design and installation of upgrades to a facility’s energy infrastructure, the design and construction of renewable energy plants, the sale of other renewable energy products and the arranging of financing for customer projects.

Energy Efficiency Services

Our services typically includes the design, engineering and installation of, and the arranging of financing for, equipment to improve the efficiency, and control the operation, of a building’s heating, ventilation, cooling and lighting systems. In certain projects, we also design and construct a central plant or cogeneration system providing power, heat and/or cooling to a building. Our projects generally range in size and scope from a one-month project to design and retrofit a lighting system to a more complex 30-month project to design and install a central plant or cogeneration system.

At the commencement of a project, we typically evaluate the customer’s energy needs and opportunities to reduce costs. We start by reviewing and analyzing the customer’s utility and other energy bills, using in complex cases our proprietary AXIS software for bill scanning and analyses. Our in-house personnel can, for example, analyze whether a customer is eligible for lower rates in a different utility rate class. Our experienced engineers then review and assess the customer’s current energy systems and determine how to optimize federal, state or local energy, utility and environmental based payments or credits available for usage reductions or renewable power generation. Upon customer approval of a project, our engineers, with the assistance in some cases of local or specialized engineers, design and engineer the project.

Energy Efficiency Measures

In designing a project for a customer, we typically include a combination of the following energy efficiency measures:

| |

• | Boilers and Furnaces. We replace low efficiency boilers and furnaces with higher efficiency equipment. In addition, to reduce emissions, we can install emissions controls or either modify existing equipment or install new equipment to use cleaner fuels. We can also install biomass boilers for customers that have access to organic materials, such as waste from agricultural or food processing activities. |

| |

• | Chillers. Small buildings are cooled by air conditioners and large buildings are cooled by chillers. We replace older low efficiency chillers with new higher efficiency chillers capable of delivering the same cooling with less energy input, often eliminating the use of atmospheric ozone depleting chlorofluorocarbon based refrigerants in the process. We retrofit existing chillers with new, more sophisticated, automated controls, high efficiency motors and variable speed drives to improve efficiency in cases where complete equipment replacement is not necessary. If the customer has an on-site source of recoverable waste heat, we may replace an electric chiller with an absorption chiller that can utilize the waste heat to directly produce cooling with reduced need to purchase energy for chiller operation. |

| |

• | Central Plants. Customers that have multiple buildings in close proximity on a site may benefit from installation of a single central plant to provide power, heat or cooling to these buildings. The central plant typically contains multiple large boilers, chillers or combined heat and power, or CHP, systems to handle the combined requirements of all site buildings. Pipes are installed to distribute steam, hot water or chilled water from the central plant to the individual buildings. Any centrally generated power is delivered via interconnection with the existing site-wide electrical distribution system. A central plant allows the multiple smaller and less energy efficient individual building heating and cooling plants to be decommissioned. In addition to improved energy efficiency, centralization can create other scale benefits in operating labor, equipment maintenance and operating reliability. Where a customer already has a central plant, we can improve the efficiency of the plant by implementing improved equipment controls and by retrofit or replacement of existing equipment for enhanced energy efficiency. |

| |

• | Cogeneration or Combined Heat and Power. CHP systems produce both heat and power simultaneously at a customer site, displacing power purchases from the utility grid and conventional sources of heat generation at the customer facility. When utilities produce power at large central station plants, the heat produced as a byproduct of the power generation process is typically wasted via disposal to the atmosphere or a nearby waterway. This wasted heat is generally a majority of the energy value of the input fuel to the power generation process. With on site power generation, the waste heat can be recovered from the power generation process and used as a substitute for heat that would otherwise be generated using site purchased fuels. Through use of heat driven chillers, also known as absorption chillers, this recovered heat can also be employed to provide building cooling. For facilities with large and relatively constant needs for power and heat or cooling, the cost of fuel for the cogeneration system operation can often be less than the cost of the purchased utility power and conventional heating fuel that is displaced. Installing a CHP that uses a lower cost fossil fuel or a renewable fuel source can create further economic benefits. |

| |

• | Energy Management Systems. Automating building system adjustments for optimum performance under changing building operating conditions is one of the most cost-effective energy saving strategies. We install energy management system, or EMS, projects consisting of small computers, wiring or wireless communication systems, and sensors and controllers located at energy using equipment and at locations that need monitoring for such conditions as temperature and flow. Equipment that may be controlled through an energy management system includes lights, boilers, chillers, and fans and pumps that move energy throughout a building. We program the computers to automatically turn the equipment on and off or to adjust equipment operating setpoints for lower energy use in response to monitored conditions. For example, when the outdoor air is cool and the building requires cooling, instead of turning on the chillers to cool the building, the EMS may turn on building fans to draw the cool outside air into the building and significantly reduce the energy use under that condition. Both we and the customer can access the EMS information through a personal computer and reprogram the energy saving strategies through secure, hardwired or web-based communications systems. |

| |

• | Lighting. We replace lighting system components with more efficient components in both indoor and outdoor lighting systems. We may alternatively redesign and install a new lighting system. Typical measures include replacing incandescent lighting with compact fluorescent lighting, metal halide lighting with fluorescent lighting and low efficiency fluorescent lighting with higher efficiency fluorescent lighting. Also, lighting controls may be installed to turn off lights when the lit space is unoccupied or if natural light through windows or skylights is adequate. |

| |

• | Retro-commissioning. Over time, the performance of building systems can degrade due to a variety of factors, such as a failure of dampers, actuators and switches to operate in accordance with the building control system or modifications to equipment without taking into account their interaction with other building systems. Cumulatively, these factors can lead to significant increased energy consumption and reduce the quality of the indoor environment. Through a retro-commissioning process, we systematically repair and restore building equipment and systems so that they function together in an optimal manner to enhance overall building performance. |

| |

• | Motors. The energy cost over the life of a motor is often many times the original cost of the motor. We replace older low efficiency motors with new higher efficiency motors. Often, motors are over sized for the application and additional savings can be attained by replacing an existing motor with an appropriately sized motor. We may also replace the sheave and belt drives associated with motors so that the motor output is transmitted to the driven device with reduced energy loss. |

| |

• | Variable Speed Drives or Variable Frequency Drives. Motors driving building equipment such as fans, pumps, chillers and elevators are typically selected and operated at the size and speed necessary to deliver services under worst case or |

peak load conditions. This causes inefficiencies when operating at less than peak load conditions. We install electronic devices called variable speed drives, or VSDs, that automatically adjust the characteristics of the power supplied to a motor so that the motor is operated at only the speed necessary to meet the load conditions at any time.

| |

• | Electric Load Shaping. Many customers pay an energy charge per kWh of electricity used and a demand charge based on their highest or peak use of electricity in a 15 minute period during the month. By installing an EMS or an on-site generator and controlling the system using our monitoring and analysis of the customer’s electricity use, we can reduce the customer’s peak electricity use and thus its demand charge. We may also shift energy use from expensive on-peak (weekday) periods to less expensive off-peak periods (nights and weekends). For example, by adding chilled water storage tanks to a facility, cooling systems can be operated at night to generate stored chilled water and the chilled water can then be withdrawn to cool the building during the next day without operating the cooling equipment during daytime peak periods. |

| |

• | Utility Rate Reductions. A customer’s cost of gas and electricity is a function of how much energy is used and what rate the customer is charged for the energy. We analyze a customer’s energy use and the various utility rates that the customer is eligible to select. By switching a customer to the optimal rate, the customer can typically save energy costs. We may be able to switch a customer into a better rate by installing an EMS or an on-site generator. |

| |

• | Geothermal Heat Pumps. Heat pumps are designed to efficiently provide both heat and cooling to a facility. The geothermal heat pump system works to store and recapture energy from the ground on a seasonally advantageous basis. Beneath the surface, the earth is warmer than the air in winter and cooler than the air in summer. Using the heat pump, heat removed from a building to cool it during the summer can be stored in the ground. This stored heat can then be withdrawn by the heat pump in the winter to provide necessary building heating. We install piping loops in the ground and heat pumps in buildings. Water piped underground captures the stored geothermal energy and heat pumps deliver the energy efficiently to the building interior. |

| |

• | Window Replacement. Existing windows are often the most inefficient component of a building envelope. We may replace existing inefficient windows with new windows with features that more effectively control the sources of window heat transfer. |

| |

• | Roofs. An existing roof with inadequate insulation levels or with water damage compromising the effectiveness of insulation is a source of unnecessary energy waste. We replace existing roofs with new roofs with higher insulation levels to reduce heat losses in winter and heat gains in summer. We may employ membrane roof technology for better protection of the insulation against degradation. |

| |

• | Insulation. Insulating materials reduce unwanted transfer of heat that can increase energy usage. We apply additional insulation to building shell components, such as walls, ceilings, floors and foundations, to reduce heat loss in winter and heat gain in summer. We may add to or fully replace existing insulation on equipment such as piping, storage tanks and heat exchangers to reduce energy losses and the equipment inefficiency that results from these losses. |

| |

• | Asset Planning. Asset planning tools enable organizations to identify and prioritize current and future facility renewal requirements and associated capital investment needs. We have developed software that helps organizations measure the condition of their facilities, the costs necessary to improve the facilities and make them more energy efficient and the funding alternatives for any such improvements. Our asset planning tools enable customers to develop facility renewal plans that will effectively leverage their available sources of capital and meet their future needs. |

| |

• | Demand Response and Demand Side Management. Electric utilities and regional or independent system operators, or ISOs, are responsible for ensuring that power is available at all times throughout a region’s electrical transmission and distribution system. It is expensive to provide power during peak times such as a hot summer afternoon when customers are turning on their air conditioners and chillers. Utilities and ISOs seek to reduce the peak load demand and are willing to pay customers to reduce their power usage at these times, either during pre-arranged hours or in response to a call to reduce power. We help utilities and ISOs to attract customers to their programs and coordinate the customers’ participation in the programs. |

| |

• | Utility Data Management. We have developed proprietary software and systems that allow us to efficiently collect, optically scan, enter into a data base and perform analysis on information from customer utility bills. Using these systems, we can deliver a variety of services, including centralized and automated collection, processing and preparation for payment of utility billing information; identification of errors in utility metering or billings; |

aggregation of multiple location billings from a single utility to facilitate payment; modeling of available utility tariff rates against a database of historical energy use to identify the most economical rate; and analysis of utility use data in multiple ways to identify and report usage and cost trends, variances and performance relative to benchmarks.

| |

• | Carbon Emissions Tracking. Our carbon management program provides greenhouse gas, or GHG, emissions accounting and reporting services to our customers. With an international, multi-tiered approach, we can support a wide variety of GHG accounting and reporting standards, including utility based GHG and full ISO 14064 compliance reporting. This service helps customers, for example, to develop corporate social responsibility reports and prepare for an audit of their GHG emissions. |

We typically purchase the equipment for our projects either from local vendors or, in certain cases, from vendors with which we have a relationship across the company. Our large volume of equipment purchases enables us to achieve cost efficiencies with our significant vendors. In most cases, we use local subcontractors to install the purchased equipment in accordance with our design and under the supervision of our project manager.

Customer Arrangements

For our energy efficiency projects, we typically enter into ESPCs under which we agree to develop, design, engineer and construct a project and also commit that the project will satisfy agreed upon performance standards that vary from project to project. These performance commitments are typically based on the design, capacity, efficiency or operation of the specific equipment and systems we install. Our commitments generally fall into three categories: pre-agreed, equipment level and whole building level. Under a pre-agreed energy reduction commitment, our customer reviews the project design in advance and agrees that, upon or shortly after completion of installation of the specified equipment comprising the project, the commitment will have been met. Under an equipment level commitment, we commit to a level of energy use reduction based on the difference in use measured first with the existing equipment and then with the replacement equipment. A whole building level commitment requires demonstration of energy usage reduction for a whole building, often based on readings of the utility meter where usage is measured. Depending on the project, the measurement and demonstration may be required only once, upon installation, based on an analysis of one or more sample installations, or may be required to be repeated at agreed upon intervals generally over periods of up to 20 years.

Under our contracts, we typically do not take responsibility for a wide variety of factors outside our control and exclude or adjust for such factors in commitment calculations. These factors include variations in energy prices and utility rates, weather, facility occupancy schedules, the amount of energy using equipment in a facility, and failure of the customer to operate or maintain the project properly. Typically, our performance commitments apply to the aggregate overall performance of a project and not to individual energy efficiency measures. Therefore, to the extent an individual measure underperforms, it may be offset by other measures that overperform during the same period. In the event that an energy efficiency project does not perform according to the agreed upon specifications, our agreements typically allow us to satisfy our obligation by adjusting or modifying the installed equipment, installing additional measures to provide substitute energy savings, or paying the customer for lost energy savings based on the assumed conditions specified in the agreement. Many of our equipment supply, local design, and installation subcontracts contain provisions that enable us to seek recourse against our vendors or subcontractors if there is a deficiency in our energy reduction commitment. From our inception to December 31, 2010, our total payments to customers and incurred costs under our energy reduction commitments, after customer acceptance of a project, have been less than $100,000 in the aggregate. See "We may have liability to our customers under our ESPCs if our projects fail to deliver the energy use reductions to which we are committed under the contract" in Item 1A, Risk Factors.

The projects that we perform for governmental agencies are governed by particular qualification and contracting regimes. Certain states require qualification with an appropriate state agency as a precondition to performing work or appearing as a qualified energy service provider for state, county and local agencies within the state. Most of the work that we perform for the federal government is performed under IDIQ agreements between government agencies and us or our subsidiaries. These IDIQ agreements allow us to contract with the relevant agencies to implement energy projects, but no work may be performed unless we and the agency agree on a task order or delivery order governing the provision of a specific project. The government agencies enter into contracts for specific projects on a competitive basis. We and our subsidiaries and affiliates are currently party to an IDIQ agreement with the U.S. Department of Energy, expiring in 2019, with an aggregate maximum potential ordering amount of $5 billion. Payments by the federal government for energy efficiency measures are based on the services provided and products installed, but are limited to the savings derived from such measures, calculated in accordance with federal regulatory guidelines and the specific contract terms. The savings are typically determined by comparing energy use and O&M costs before and after the installation of the energy efficiency measures, adjusted for changes that affect energy use

and O&M costs but are not caused by the energy efficiency measures.

Engineering and Installation Controls

Our engineering and construction quality, schedule and budget goals are managed through several control processes. We follow formal processes for the review and approval of the technical and economic content of all proposals by senior managers. Our engineers employ standardized, and in some cases proprietary, software tools for technical and economic analysis to establish a baseline for quality and accuracy during the development stage of our projects. We fully review final design, engineering and construction document preparation efforts at selected milestones, using internal or subcontracted specialized engineering resources. During the construction phase, a construction project management team utilizes a number of tools to manage quality, cost and schedule. We use agreement templates, customized to meet the specific technical requirements of each project, to ensure well defined procedures and responsibilities to be followed by our equipment suppliers and labor subcontractors. We use scheduling software to prepare, regularly update and communicate project schedules at a task specific level. Inspections of work progress and quality are conducted throughout the construction process at frequent intervals. Both project managers and senior management use a computerized project control system throughout the project delivery process to track actual project costs against project budgets on a real-time basis. In addition, we employ a full-time, dedicated safety director who is responsible for developing and promulgating best practices and training throughout the organization and working with our regional safety coordinators to ensure appropriate procedures are in place at all job sites.

Operations and Maintenance Services

After a project is completed, we often provide ongoing O&M services under a multi-year contract. These services include operating, maintaining and repairing facility energy systems such as boilers, chillers and building controls, as well as central power plants. For larger projects, we often maintain staff on-site to perform these services.

Renewable Energy Projects and Products

Our services offering includes the development, construction and operation of, and the arrangement of financing for, small-scale renewable energy plants, as well as the sale and integration of solar energy products and systems.

We have constructed and are currently designing and constructing a wide range of renewable energy plants using LFG, wastewater treatment biogas, solar, wind, biomass, food waste, animal waste and hydro sources of energy. Most of our renewable energy projects to date have involved the generation of electricity from LFG or the sale of processed LFG. LFG is created by the action of micro-organisms within a landfill that generate methane gas as a byproduct of solid waste decay. Generally, landfills avoid the unsafe build up of methane-containing LFG by venting it into the atmosphere, or in most cases, by collecting and flaring it. As methane is suspected of contributing to global climate change and is regulated as a pollutant, landfill owners are generally required by environmental laws to collect and combust LFG, usually in a flare. We purchase the LFG that otherwise would be combusted or vented, process it, and either sell it or use it in our energy plants. Electricity that we sell is generally delivered to the customer at the interconnection of our plant with the electrical grid. The thermal energy that we sell is generally delivered to the customer at the inlet flange of the thermal piping located at the customer's facilities. The processed LFG we sell to industrial customers is generally delivered by us to the customer's facility through a pipeline transmission system that we design, construct and operate. Under our energy supply agreements, we typically provide all environmental attributes associated with the project, including those represented by renewable energy certificates, to the customer.

Depending on the customer's preference, we will either build, own and operate the completed plant or build it for the customer to own. We generally sell the electricity, gas, heat or cooling generated by small-scale plants that we own under long-term contracts, typically to utilities, industrial facilities or other large users of energy. For an LFG plant, the output will typically be sold under a sales agreement with a term covering ten to 20 years of plant operation. The right to use the site for the energy plant, and the purchase of the renewable energy needed to fuel the plant, are also obtained under long-term agreements with terms at least as long as that of the associated output sales agreement. Our projects are generally designed and permitted by our own engineers, although we often obtain additional engineering assistance from consulting engineers. We generally subcontract installation of project equipment, under the supervision of our construction manager.

As part of our renewable energy offering, we also distribute and integrate solar energy products manufactured by several vendors. We are a distributor of PV panels, solar regulators, solar charge controllers, inverters, solar powered lighting systems, solar powered water pumps, solar panel mounting hardware and other system components. We also integrate our PV products and system components into solar solutions designed specifically for customers. We provide solar energy solutions for both on-

grid applications where the solar power is used in a building connected to a utility distribution system, and for off-grid applications where the power is used directly in the device using the electricity, such as traffic signs.

We also design and construct renewable energy plants based on wind power. In many parts of the country, available wind resources, utility net metering and local incentives can make on-site wind generation a viable solution for meeting a significant portion of customers' energy needs. As of December 31, 2010, 2010, we had completed two projects that included a wind turbine.

In addition, we have constructed, and are constructing, small-scale renewable energy plants based on biomass. Biomass is organic material such as wood, agricultural waste, animal waste and waste from food processors. Biomass is typically converted to energy by burning or gasifying it in a boiler to produce steam or gas. Our largest renewable energy plant is currently under construction and will use biomass as the primary source of energy.

As of December 31, 2010, we had constructed more than 28 renewable energy projects, and owned and operated 22 small-scale renewable energy plants. Of the owned plants, 19 are renewable LFG plants, two are waste water biogas plants, and one is a solar PV installation. These 22 small-scale renewable energy plants have the capacity to generate electricity or deliver LFG producing an aggregate of 106 megawatts (MW) or megawatt-equivalents (MWE). As of December 31, 2010, we had signed contracts for the construction, operation and ownership of an additional six LFG plants, two biomass power and cogeneration plants and five biomass boiler projects. If and when completed, we expect that the LFG plants will be capable of producing an aggregate of approximately 27 MW or MWE, the biomass power and cogeneration plants will be capable of producing approximately 21 MW, and the biomass boiler projects will be capable of producing approximately 41 million BTU per hour of steam or hot water.

Examples of Energy Efficiency and Renewable Energy Projects

The following are examples of energy efficiency and renewable energy projects we have designed and either have installed or are installing for customers. While most of our projects are less complex and smaller in scope than those shown below, these examples are intended to demonstrate how various different types of energy efficiency measures and renewable energy plants can be combined to create a customized solution addressing the multiple needs of a customer.

Elmendorf Air Force Base (Alaska). Elmendorf Air Force Base had an inefficient, costly-to-operate central heating and power plant and approximately 50 miles of aging steam and condensate distribution piping. We modernized the heating system by demolishing the central plant and installing over 200 boilers and 20 alternate heating systems in over 120 commercial facilities. We worked with the local gas utility to install approximately seven miles of gas pipeline to serve the new, decentralized boilers and negotiated a new gas and electric service for the Base with the local utilities. We also installed over 800 energy efficient steam traps and abated over 125 steam pits throughout the base. The $49 million project is designed to save approximately $4 million of energy and energy-related O&M costs per year. This work was completed in 2008. We provide a full-time staff of four people at the base and have contracted to perform approximately $22 million of fixed price O&M services throughout the 22-year performance period term of our agreement.

Hill Air Force Base (Utah). Hill Air Force Base was seeking to upgrade its inefficient energy systems and maximize the use of renewable energy sources including using gas from an off-base landfill to lower its energy costs. In response, during the period from 2005 to 2009, we designed and installed $18.0 million of energy efficiency and renewable energy projects which are designed to save approximately $2.1 million of energy costs per year. The energy efficiency projects include the installation of a wide range of high efficiency lighting, heating and cooling systems and associated controls for these and other energy-consuming equipment. The Base also provides compressed air, steam, water cooling and wastewater treatment services to a nearby industrial area. We upgraded and control these systems to reduce the disposal of hazardous materials and the loss of steam, water and electricity. The renewable energy projects include a 210 kW ground-mounted solar PV array and an LFG project involving the purchase of gas from the Davis County landfill, piping the gas over one mile to the base, processing the gas and producing approximately 2.25 MW of power. We operate and maintain the LFG project, the PV project, and the steam traps in the heating distribution system with an on-site operator and the remote support of two engineers for a fixed price of $1.1 million per year under a 20 year contract. We believe the PV system was the largest in Utah at the time it was installed.

State of Missouri Correctional Facilities. The State of Missouri and Columbia Water & Light were seeking to lower and stabilize their energy costs by purchasing thermal energy and electricity, respectively, from a cogeneration facility fueled by LFG from the Jefferson City Landfill owned by a subsidiary of Republic Services, Inc. The State of Missouri also wanted to upgrade its inefficient energy systems at two state-owned correctional facilities, Algoa and Jefferson City. In 2009 we completed the design and installation of $8.4 million of energy efficiency improvements and the design, financing and

installation of a 3.2 MW $7.2 million cogeneration facility, which together are designed to save approximately $0.7 million of energy costs per year. The energy efficiency measures include the installation of high efficiency lighting systems, electrical system improvements, steam traps to reduce steam losses and controls for various energy-using equipment within the correctional facilities. The LFG project, which we own, purchases LFG from Republic, processes the gas and then pipes it approximately three miles to the Jefferson City Correctional Facility to use as a fuel source in our cogeneration facility that produces electricity and thermal energy. Columbia Water & Light purchases the power at a fixed rate per kWh for all electricity that is delivered. The State of Missouri has a take or pay obligation for a minimum amount of thermal energy at a fixed price.

Porta Community Unit School District (Illinois). Porta Community Unit School District #202 was seeking to lower and stabilize its operating costs and improve its educational environment. To achieve this goal, we designed, installed and completed in 2009 a $7.6 million energy efficiency and renewable energy project, which is designed to save over $0.4 million of energy and operating costs per year. The project includes energy efficient lighting retrofits, recommissioning and upgrade of the existing heating, ventilation and air conditioning control system, domestic hot water system upgrades and swimming pool heating system upgrades. The project also includes the design and construction of a geothermal heating and cooling system to heat and cool the building. In addition, we installed a one kW PV energy system and a 600 kW wind energy generating system. When the wind turbine generates more electricity than the district can use, the excess electricity is sold to the local utility under a net metering arrangement. We believe the district is the first school district in Illinois to employ a combination of geothermal, solar and wind renewable technologies.

BMW (South Carolina). BMW was seeking to lower and stabilize its energy costs, and Waste Management was seeking to monetize the value of the LFG produced at its Palmetto Landfill. To achieve these goals, in 2003, we completed the development, design, construction and financing for the $9.6 million project to process and deliver LFG to BMW's factory and refurbish BMW's boilers and turbines to be able to utilize the LFG fuel. BMW also uses the LFG to provide energy for its paint shop, incinerator and pollution control devices. This project involves buying LFG from Waste Management at its Palmetto Landfill, processing and compressing the LFG adjacent to the landfill and piping the LFG approximately 9.5 miles for delivery to BMW. Over the period from 2005 to 2009, the project has delivered from 0.88 to 1.17 million BTU annually. BMW pays for the LFG under a multi-year supply contract. Our delivery obligations are limited to those volumes of LFG supplied to us by Waste Management. In 2009, BMW announced that the project produces over 60% of the plant's total energy requirements, saving BMW an average of $5 million in energy costs annually while reducing carbon dioxide emissions by approximately 92,000 tons per year.

U.S. Department of Energy Savannah River Site (South Carolina). The Savannah River Site, or SRS, utilizes steam and power for process and heating loads currently generated from an aging and inefficient coal power plant. We are currently constructing a 20.7 MW cogeneration plant to replace this coal power plant. The cogeneration plant will use fuel from forest residue, scrap tires, pallets and other clean wood and is scheduled to come on line in December 2011. We will install two ten million BTU per hour wood-fired heating plants at other SRS locations to replace an old and inefficient fuel oil heating plant. These smaller plants are scheduled to come online in November 2010. This $183.4 million project is designed to save approximately $34 million of energy and energy related O&M costs per year. We will provide a full time staff of 20 to 25 people at the new plant and have contracted to perform approximately $17 million of O&M services annually, at escalating fixed rates, throughout the 19-year performance period of the agreement.

City of Vancouver (British Columbia, Canada). The City of Vancouver was seeking to implement a comprehensive greenhouse gas reduction project in its larger facilities. From 2006 to 2010, we designed and installed two phases of work, with an additional third phase expected to be completed by October 2010. This comprehensive $14.7 million energy efficiency and facility renewal project includes boiler plant replacements in 18 facilities, comprehensive lighting upgrades, HVAC upgrades, solar hot water, desiccant dehumidification and low-emissivity ceilings and heat recovery in ice rinks. The project is designed to save $0.9 million per year in energy costs.

Sales and Marketing